If you’re looking to start a business, or need capital to help grow and expand your current business, there are a multitude of loan options available. Even if you don’t have the best credit rating, and your business is too new to have one of its own, you still have options.

Small Business Administration (SBA) loans

The SBA offers a number of loan programs–from general loans to real estate and equipment and disaster loans. There’s even a microloan program that provides small, short-term loans of up to $50,000.

The SBA does not give the loan directly to you. It works with lenders and other partners to guarantee the funds will be repaid, reducing the lender’s risk. This video from the SBA explains its most popular 7(a) loan:

Use the SBA search tool to find lenders in your area. Loan amounts can be as high as $5 million, with interest rates ranging from 4% to 10%, and terms up to 25 years. Loans can be used to start, acquire, or expand a business, purchase property, refinance debt, or recover from disasters.

Leo Welder's SlideShare "Guide to Small Business Administration Loans," provides details on other types of SBA loans and allowed uses for the money borrowed.

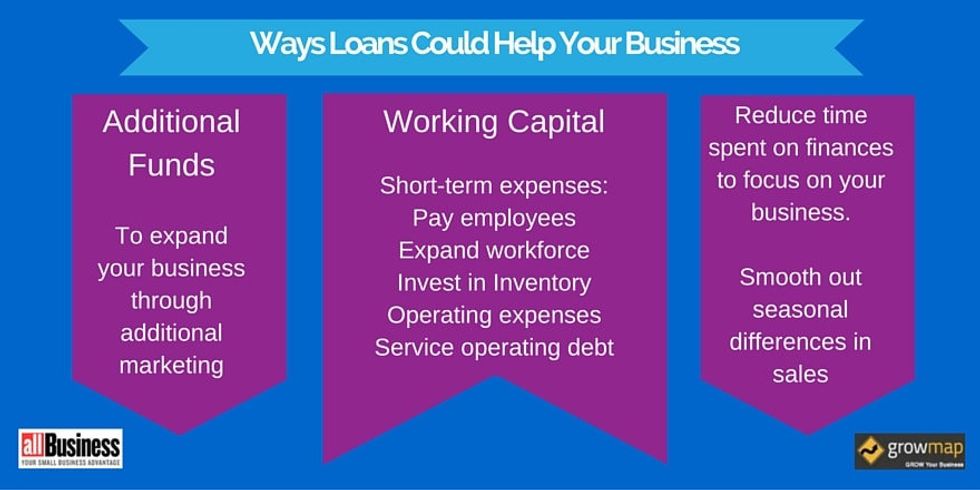

Working capital/short-term loans

According to the SBA, working capital is the difference between your assets and liabilities. Your assets should be cash or what you can quickly convert to cash; your liabilities are debts or obligations due within a year.

So, let’s say you’ve got $50,000 in current liquid assets and $25,000 in current liabilities. Your business has positive working capital, so it’s able to meet operational needs. Without that positive working capital, your business runs the risk of failing to meet obligations on time.

A working capital loan is meant to provide financing for everyday operations. It’s designed to help pay employees, taxes, and similar debts, rather than buy long-term investments or assets.

Working capital loans are available through a number of lenders. Some may require collateral, while others may not, depending on your financial standing and credit history. Typically, unsecured loans (those without collateral) will come at a higher interest rate.

Some lenders, like PayPal, may not require a credit check. Instead, they rely on your sales history and let you choose the repayment terms that will work for you. You’ll pay a percentage of each sale your business makes through PayPal until the loan is paid off. And, if you think you can avoid repayment by funneling money away from PayPal, a certain amount is due every month anyway.

If your business opts for a short-term loan, make sure you clearly understand the terms and conditions of the loan. Short-term loans are often the most expensive borrowing route, so use them only as a last resort, or when you know you can repay the loan quickly to avoid paying a large amount of interest. Even though interest rates are higher for short-term loans, they are still usually cheaper than credit cards.

Be aware that the laws governing short-term loans are different in the UK versus the U.S., with the UK providing more borrower protections. While still expensive, short-term small business loans also can have lower interest rates than payday-type loans.

Understanding the difference between payday, short-term, and what are referred to as “quick” loans can prevent the imposition of costly additional fees. Be sure to read the fine print and know what your country permits. Some countries have greater protections against onerous interest rates than others.

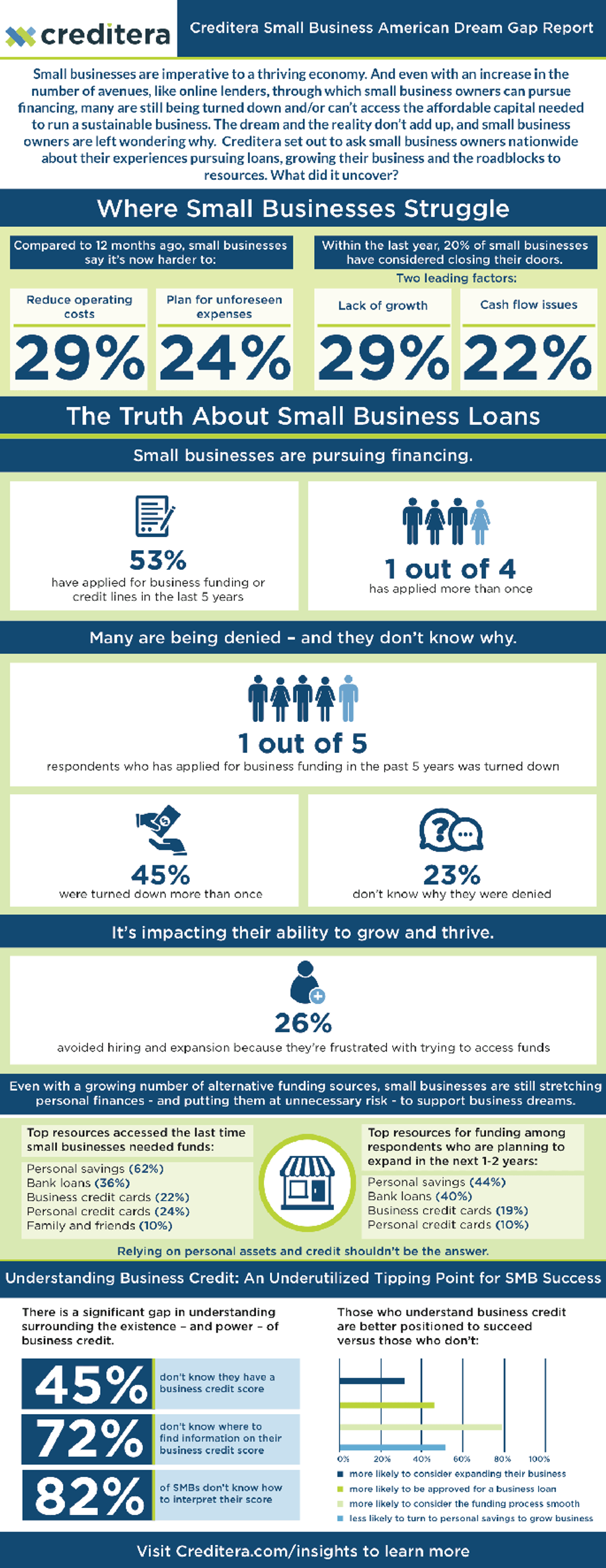

Why many small businesses struggle to get loans

A small business survey by Nav reported:

Forty-five percent of small business owners who are denied financing get turned down more than once and 23% don’t know why their applications were denied.

Nav analyzed why and compiled the findings in the infographic below. (Click the image to read the full report.)

Invoice advances

For many small business owners, cash flow is an issue. It’s especially frustrating when you know you have thousands of dollars of work completed and invoiced, but you’re sitting with zero dollars in your account, bills are due, and payroll needs to be met.

Services like Fundbox and Invoice Advance will pay your verified invoices for you. Depending on the lender, you’ll either get a portion of the invoice and the remainder minus a fee when it is actually paid, or you’ll get the entire amount and will need to pay a fee over a number of weeks.

Small business loans with no credit

Don’t be surprised if most banks insist on at least two years of perfect credit history for you to qualify for a loan. According to Mulligan Funding in "How to Get a Small Business Loan With No Credit":

The real reason behind the dramatic reduction in bank business loans since 2008 (i.e., when the Great Recession erupted), is that banks themselves have made it virtually impossible for small business owners to qualify for a business loan unless they have both a long and perfect credit history."

There are alternatives to traditional banks for both working capital loans and conventional loans explained in a downloadable guide in that post. It explains why working capital loans can be safer than conventional business loans.

Home equity lines of credit (HELOC)

Business owners who are unable to qualify for any other type of loan will sometimes use a home equity line of credit (HELOC) to cover operating costs or emergency expenses. Think carefully before going this route, as you could end up losing both your business and your home.

A HELOC provides a revolving line or credit similar to a credit card using your home as the collateral. You are literally risking your home to cover business expenses, with the upside being a lower monthly payment and interest rate than your business might be able to obtain. Changes in the variable interest rate and real estate market can affect costs and increase risks.

Make sure you understand all the pros and cons before taking out a HELOC. The recent post "Is It Wise to Rely on HELOC For a Financial Emergency" contains extensive information on this type of financing.

Loan comparison tools

Regardless of the kind of loan your small business is seeking, a loan comparison tool can help speed up the application process. With a side-by-side look at lenders, origination fees, and interest rates, you can quickly and easily determine which, if any, lenders have terms you find acceptable. Many businesses give up after three or four lenders, but George Cloutier, CEO of American Management Services, suggests it is a good idea to try up to 10.

Before applying for loans anywhere, do your homework. Make sure you have proof of income, or at the very least, a business plan to show how you plan to earn income. Be prepared to provide personal income documentation to support the business loan.

Know what you’re going to use the loan for, and have a good idea of when you’ll be able to pay it back. And as mentioned before, know your business credit score which is separate from your personal credit score. This will help you choose the best lender for your needs.

Now that you know what kinds of loans are available, seriously think about whether you actually need one. Here is what entrepreneur Mark Cuban has to say about starting a business on a loan: